Does Homeowners Insurance Cover Roof Replacement? 2026 Guide (PA, WV, OH)

Storm or hail just hit your roof? The first question on every homeowner's mind is: does homeowners insurance cover roof replacement? This 2026 guide explains exactly what's covered, how ACV vs RCV affects your payout, deductibles, and how to file a successful claim in PA, WV, and OH.

A roof insurance claim can be the difference between paying $15,000 out of pocket and paying only your deductible. But the rules around coverage, depreciation, and deadlines confuse most homeowners, and a single mistake can get your claim denied. This guide breaks it all down in plain English.

At Tri-Link Contracting Services, our veteran-owned team has helped thousands of homeowners across Pittsburgh, Washington County, Allegheny County, Morgantown WV, and Wheeling WV document storm damage and navigate the claims process honestly and successfully. Here's what you need to know.

- Insurance covers roof replacement from covered perils like wind, hail, fire, and fallen trees

- It does NOT cover normal wear, age, or poor maintenance

- RCV pays full replacement minus deductible; ACV pays minus depreciation

- Roofs over 15-20 years are often limited to ACV-only coverage

- File promptly and document everything - Tri-Link helps for free

Does Insurance Cover Roof Replacement? The Short Answer

Yes - homeowners insurance typically covers roof replacement when the damage is caused by a sudden, accidental event known as a "covered peril." This includes wind, hail, fire, lightning, falling trees, and vandalism. If a storm rips off your shingles or hail punctures your roof, your policy is designed to help.

What insurance does not cover is gradual damage: normal wear and tear, an old worn-out roof, poor maintenance, or manufacturer defects. Insurance is for sudden losses, not for replacing a roof that simply reached the end of its life. If you're unsure whether your roof is storm-damaged or just aging, a free storm damage inspection will give you a clear answer.

What Roof Damage Is Covered (and What Isn't)

Here's a clear breakdown of what most standard homeowners policies cover and exclude:

| Usually Covered | Usually NOT Covered |

|---|---|

| Wind and storm damage | Normal wear and tear |

| Hail damage | Age-related deterioration |

| Fire and lightning | Poor or deferred maintenance |

| Fallen trees or limbs | Improper installation |

| Vandalism | Manufacturer defects |

| Weight of ice or snow | Flood or earthquake (separate policy) |

Damage from floods and earthquakes is excluded from standard homeowners policies. If you live in a flood-prone area, you need separate coverage.

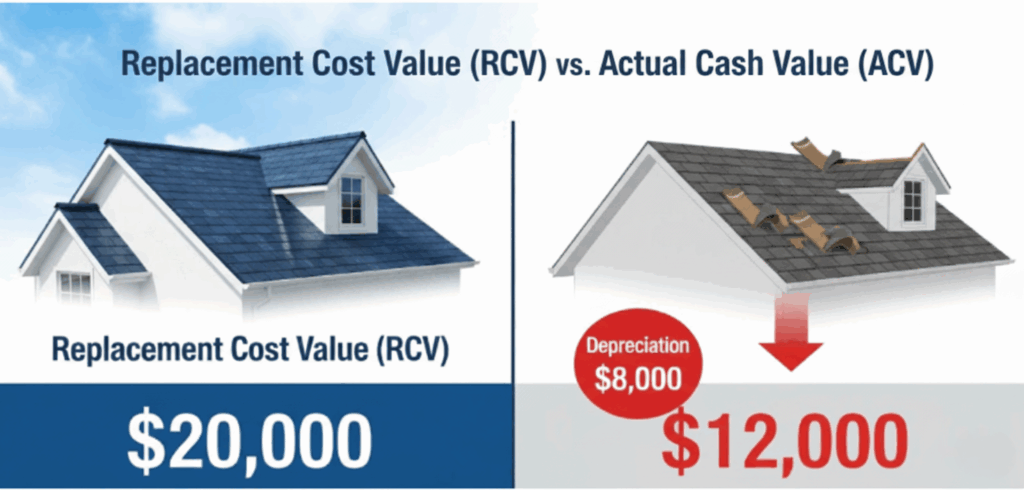

ACV vs RCV: How Much Will Insurance Actually Pay?

This is the single most important factor in your payout. Your policy pays out based on one of two methods, and the difference can be thousands of dollars.

Replacement Cost Value (RCV)

RCV coverage pays the full cost to replace your roof with new materials of the same type and quality, minus only your deductible - regardless of how old your roof is. Most homeowners have RCV policies, and it's the better coverage for a full payout.

Actual Cash Value (ACV)

ACV coverage pays the replacement cost minus depreciation. The older your roof, the less you receive. A 20-year-old roof may have lost most of its value, leaving you to cover the majority of the replacement yourself.

A Real Example

Say a storm destroys your roof and replacement costs $15,000, with a $2,000 deductible:

| Coverage Type | How It's Calculated | Your Payout |

|---|---|---|

| RCV Policy | $15,000 - $2,000 deductible | $13,000 |

| ACV (newer roof) | $15,000 - $3,000 depreciation - $2,000 | $10,000 |

| ACV (20-yr-old roof) | $15,000 - $11,000 depreciation - $2,000 | $2,000 |

Check your policy's declaration page to see whether you have RCV or ACV coverage before a storm hits. It's one of the most valuable things you can know as a homeowner.

Understanding Your Deductible

Your deductible is the amount you pay out of pocket before insurance covers the rest. If your roof replacement is $15,000 and your deductible is $2,000, insurance pays up to $13,000 (on an RCV policy) and you pay the $2,000.

Many policies also have a separate wind and hail deductible, often calculated as a percentage of your home's insured value (commonly 1-5%) rather than a flat dollar amount. On a $300,000 home, a 2% wind/hail deductible means $6,000 out of pocket - so always check this number.

If a contractor offers to "waive" or "pay" your deductible, walk away. This is illegal in many states and is a major red flag for insurance fraud. A reputable contractor like Tri-Link will never ask you to do anything dishonest.

How Roof Age Affects Your Claim

Roof age is one of the biggest factors insurers look at:

- Under 10 years: Usually full RCV coverage and the smoothest claims

- 10-15 years: Many insurers begin switching to ACV-only coverage

- 15-20 years: ACV is common, and depreciation significantly cuts payouts

- Over 20 years: Coverage may be limited, reduced, or excluded entirely

If your roof is older and showing its age, it helps to know the warning signs you need a new roof and review our full roof replacement guide to plan ahead.

How to File a Roof Insurance Claim: Step by Step

Follow these steps to give your claim the best chance of approval:

Step 1: Document the Damage

Take clear, dated photos of all visible damage from the ground. If you have older photos showing your roof in good condition before the storm, save those too.

Step 2: Get a Professional Inspection

Have a licensed roofer like Tri-Link perform a free storm damage inspection. We identify damage you can't see from the ground and provide a detailed report.

Step 3: Review Your Policy

Check whether you have ACV or RCV coverage, your deductible, your wind/hail deductible, and your filing deadline.

Step 4: File Promptly

Contact your insurer as soon as possible. Most policies have a strict filing window after the damage event, so don't wait.

Step 5: Meet the Adjuster

When the insurance adjuster inspects your roof, it helps to have your contractor present to point out all the damage and ensure nothing is missed.

Step 6: Get the Work Done Right

Once approved, choose a licensed, insured contractor to complete the replacement properly and provide the documentation your insurer needs to release final payment.

Common Reasons Roof Claims Get Denied

Avoid these pitfalls that lead to denied or reduced claims:

- Damage ruled wear and tear: The most common denial - insurers say the roof was simply old

- Missed filing deadline: Waiting too long after the storm

- Old roof on ACV coverage: Depreciation wipes out most of the payout

- Insufficient documentation: Not enough photos or proof of the damage

- Damage below the deductible: Repair cost is less than what you'd pay anyway

- Pre-existing or unrepaired damage: Issues that existed before the covered event

How Tri-Link Helps With Your Insurance Claim

A good contractor is your biggest asset in a roof claim. Here's how Tri-Link supports you honestly through the storm damage process:

- Free, thorough inspection to document all storm and hail damage

- Detailed damage report and photos for your insurance file

- We can meet your adjuster so no legitimate damage is overlooked

- Accurate, code-compliant estimates the insurer can rely on

- Quality installation with the documentation needed to release final payment

- Honest guidance - if you don't have a valid claim, we'll tell you

We never inflate claims or encourage fraud. Our reputation across PA, WV, and OH is built on doing right by homeowners and insurers alike.

Mistakes to Avoid During a Roof Claim

1. Waiting Too Long to File

Storm damage worsens over time and you can miss your policy deadline. Inspect and file promptly.

2. Signing With "Storm Chasers"

Out-of-town crews that appear after a storm often do poor work and vanish. Choose a local, established contractor with a real address and reviews.

3. Accepting the First Estimate Blindly

Adjusters sometimes miss damage. A professional contractor inspection ensures the full, legitimate scope is captured.

4. Doing Temporary Repairs and Forgetting

Tarp the roof to prevent further damage, but document everything first and complete permanent repairs properly.

Why Choose Tri-Link Contracting

When it comes to storm damage and insurance claims, experience and integrity matter. Here's why homeowners across Pittsburgh, Washington County, Allegheny County, Morgantown WV, Wheeling WV, and Cuyahoga County OH trust Tri-Link.

- Veteran owned and operated with military discipline and honest work

- 15+ years of experience handling storm and insurance work across PA, WV, and OH

- A+ BBB rating and trusted by the Better Business Bureau

- 4.9-star Google reviews based on 110+ verified customers

- Free storm damage inspections with no high-pressure sales

- Honest claim guidance - never fraud, never inflated estimates

- 0% financing available to cover your deductible or any gap

Storm Damage? Get a Free Inspection Today.

Find out if you have a valid roof claim from the most trusted veteran-owned roofing team in PA, WV, and OH. Honest answers, no pressure, no surprises.

Final Thoughts

So, does homeowners insurance cover roof replacement? Yes - when the damage comes from a covered peril like wind, hail, fire, or a fallen tree. The key is understanding your ACV vs RCV coverage, your deductible, your roof's age, and filing promptly with solid documentation.

The right contractor makes the whole process easier and more successful. Tri-Link Contracting has helped homeowners across Pittsburgh, Washington County, Allegheny County, Morgantown WV, Wheeling WV, and Cuyahoga County OH document damage and navigate claims honestly for over 15 years.

Think you have storm damage? Call us at 724-470-7669 or request your free inspection online.

Frequently Asked Questions

Have more questions about roof insurance claims? Here are the most common questions we hear from homeowners across PA, WV, and OH.

Yes, homeowners insurance typically covers roof replacement when the damage is caused by a covered peril like wind, hail, fire, lightning, or a fallen tree. It does not cover normal wear and tear, age-related deterioration, or poor maintenance. A free inspection can confirm whether your damage qualifies.

Replacement Cost Value (RCV) pays the full cost to replace your roof minus your deductible, regardless of age. Actual Cash Value (ACV) pays the replacement cost minus depreciation, so older roofs receive much smaller payouts. Check your policy's declaration page to see which you have.

Most policies require you to file within a set window after the damage occurs, often ranging from a few months up to one year. File as soon as possible after the storm and check your specific policy for the exact deadline, because missing it can void your claim.

Yes. Many insurers switch roofs over 15 to 20 years old to ACV-only coverage or limit coverage entirely, which significantly reduces your payout due to depreciation. Newer roofs generally qualify for full replacement cost coverage.

It can. Claims for covered storm or hail damage are common and often justified, but filing multiple claims over time may affect your premium. For minor damage close to your deductible, weigh the payout against the cost before filing.

The deductible is the amount you pay out of pocket before insurance covers the rest. Many policies also have a separate, percentage-based deductible for wind and hail damage, which can be significantly higher than your standard deductible.

Common reasons include damage classified as wear and tear, an old or poorly maintained roof, missing the filing deadline, insufficient documentation, or damage below your deductible amount. A professional inspection and proper documentation greatly improve your chances of approval.

We serve Pittsburgh, Canonsburg, Bridgeville, Washington County, Allegheny County, Westmoreland County, Morgantown WV, Wheeling WV, northern West Virginia, Cuyahoga County OH, Lorain County OH, and surrounding areas.